The Employee's Provident Fund (EPF) remains India's most trusted

retirement savings tool offering steady returns, tax benefits, and employer contributions.

Learn how EPF works, new 2025 withdrawal rules, and how to maximize its long-term benefits

for a secure retirement.

EPF: India's Trusted Retirement Savings Scheme

For most salaried Indians, the Employees' Provident Fund or EPF is where retirement planning

quietly begins. It's not a flashy investment, nor does it promise market-linked highs, but its

strength lies in something far more enduring: reliability. Established under the Employees'

Provident Fund & Miscellaneous Provisions Act, EPF has for decades served as India's most trusted

retirement savings vehicle blending steady compounding, tax benefits, and employer participation

into one disciplined structure.

According to EPFO data, over 6 crore salaried Indians actively contribute to EPF each month,

collectively managing one of the largest pension-linked pools in Asia. What makes it special is that

it enforces a habit that most people struggle to build voluntarily, consistent, long-term saving.

Each month's contribution may seem small, but over decades, it transforms into a meaningful corpus

that supports your post-retirement life.

How EPF Works: The Basic

Construct

The Employees' Provident Fund (EPF) isn't just one single scheme;

It's actually made up of three parts, each serving a different purpose.

The 1st component is the Provident Fund itself, which

helps you

build a retirement nest egg. This is the savings and wealth creation part of the scheme.

The 2nd component is the Employee Pension Scheme (EPS).

This is

designed to provide you with a steady pension once you turn 58, ensuring you have

financial support after retirement.

The 3rd component is the Employees' Deposit Linked Insurance

Scheme

(EDLI), which offers life insurance coverage to protect your loved ones in

case

something happens to you.

The best part?

You don't need to sign up for each of these

separately.

As soon as you're registered under EPF, you're automatically covered under EPS and

EDLI too.

Now, let's break down how each component of the

EPF contributes to your

salary.

At its core, the Employees' Provident Fund (EPF) is a structured savings plan where both you and your

employer contribute a fixed percentage of your salary every month. These contributions are mainly

invested in secure, government-backed instruments, which offer safety and stable long-term returns.

Each year, interest is added to your accumulated balance. The current rate is

around

8 to 8.25 percent p.a

While this rate might seem modest, the real magic lies in compounding. Over

time,

consistent

contributions and employer matching can lead to impressive growth. For instance, a 30-year-old who

contributes ₹10,000 a month (with an equal contribution from the employer) could build a retirement

corpus of about ₹80 - 90 lakh by age 60. To see how pushing your savings timeline back affects your ultimate

nest egg, check out the Cost of Delay

Calculator.

How an EPF Account is Created

For most salaried employees, starting an EPF account is effortless because it happens automatically.

When you join an eligible organization (typically one with 20 or more employees), your employer

registers you with the Employees' Provident Fund Organisation (EPFO). A unique Universal Account

Number

(UAN) is generated for you, and this number remains the same throughout your working life. Each new

employer simply links your UAN to their establishment's PF account, ensuring continuity as you

switch

jobs.

You can activate your UAN through the EPFO Member e-Sewa portal, which allows you to track your

contributions, interest earned, and total balance. This digital framework has made EPF management

transparent and easy to monitor - something earlier generations of employees never had.

Eligibility and Coverage

EPF coverage is wide and automatic. Any salaried employee working in an organization

registered under the EPFO and earning up to ₹15,000 per month is

mandatorily covered.

Those earning more can voluntarily opt in to continue the benefit.

Applicable to employees aged 18 to 58 years

Contributions are automatically deducted and credited to your EPF account

Your account remains portable across employers, ensuring continuity through job changes

This portability is one of EPF's most underrated advantages: it

allows uninterrupted corpus

growth through an entire career, regardless of how many times you switch jobs.

How to Transfer your EPF

when changing jobs

One of EPF's most valuable features is that it travels with you. Whenever you change jobs, your

savings don't remain stuck with your old employer they can be smoothly transferred to your new

account linked under the same UAN.

To transfer online, log in to the EPFO Member e-Sewa portal, go to

“Online

Services,” and

select “One Member - One EPF Account (Transfer Request).” You'll need to verify your

previous and current employer details, choose who will authenticate the transfer, and confirm via

Aadhaar-based OTP. Once approved, the funds are electronically shifted to your new account.

This simple process keeps your entire EPF history consolidated under one number, ensuring

uninterrupted interest accrual and making future withdrawals hassle-free. If the online route

doesn't work, you can always use Form 13 for an offline transfer through your current employer.

Step 1 Check UAN Activation

Ensure your Universal Account Number (UAN) is active.

Verify that your KYC details are approved by your previous employer.

Step 2 Link Old & New PF Accounts

Your UAN remains the same across jobs.

When you join a new company, provide the same UAN.

The new employer will link your new PF account with your existing

UAN.

Step 3 Initiate online transfer request

Log in to the UAN Member Portal. Go to Online Services → One Member

- One EPF Account (Transfer Request)

Select the PF account from which you want to transfer (old

employer).

Choose either previous employer or present employer to attest the

transfer request.

Generally, choosing the current employer speeds up

approval.

Step 4 Submit transfer request

After submitting, an OTP is sent to your registered mobile (linked

with Aadhaar).

Authenticate with OTP to complete submission.

You will get a tracking ID to monitor progress.

Step 5 Employer verification request

The chosen employer (old or new) verifies your request digitally.

Once verified, EPFO starts processing the transfer.

Step 6 Transfer completion

EPFO moves your PF balance + service history from the old account to

the new one.

You can track the status under Track Claim Status in the portal.

After completion, you'll receive an SMS notification, and the

updated balance will reflect in the passbook.

EPF

Contributions and

Compounding

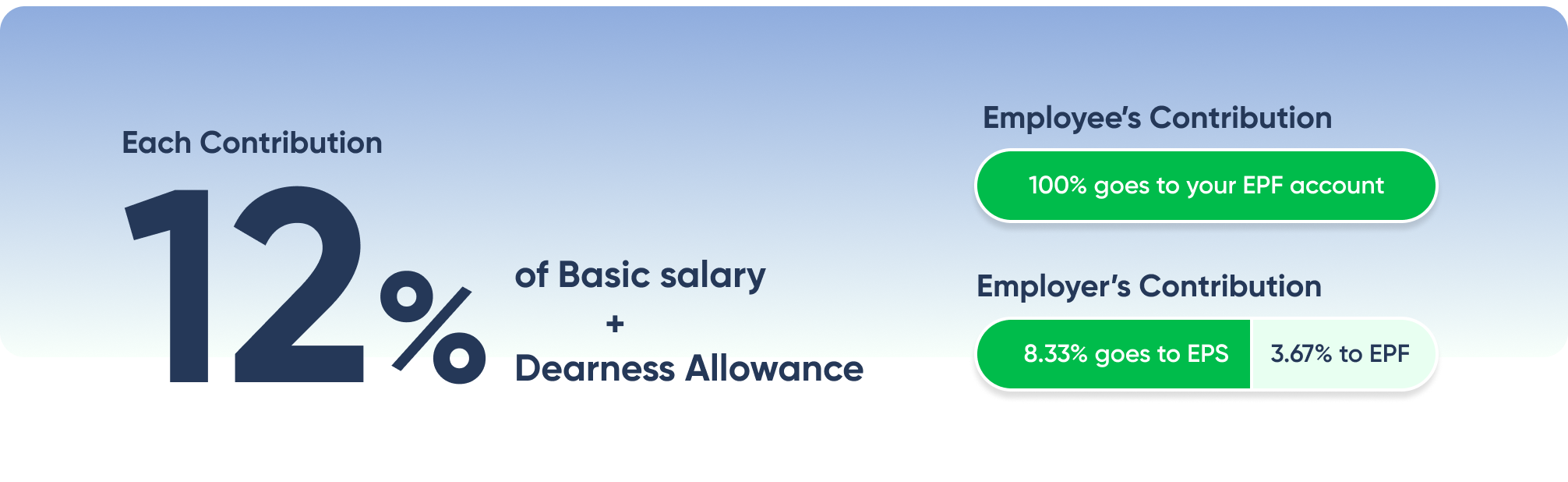

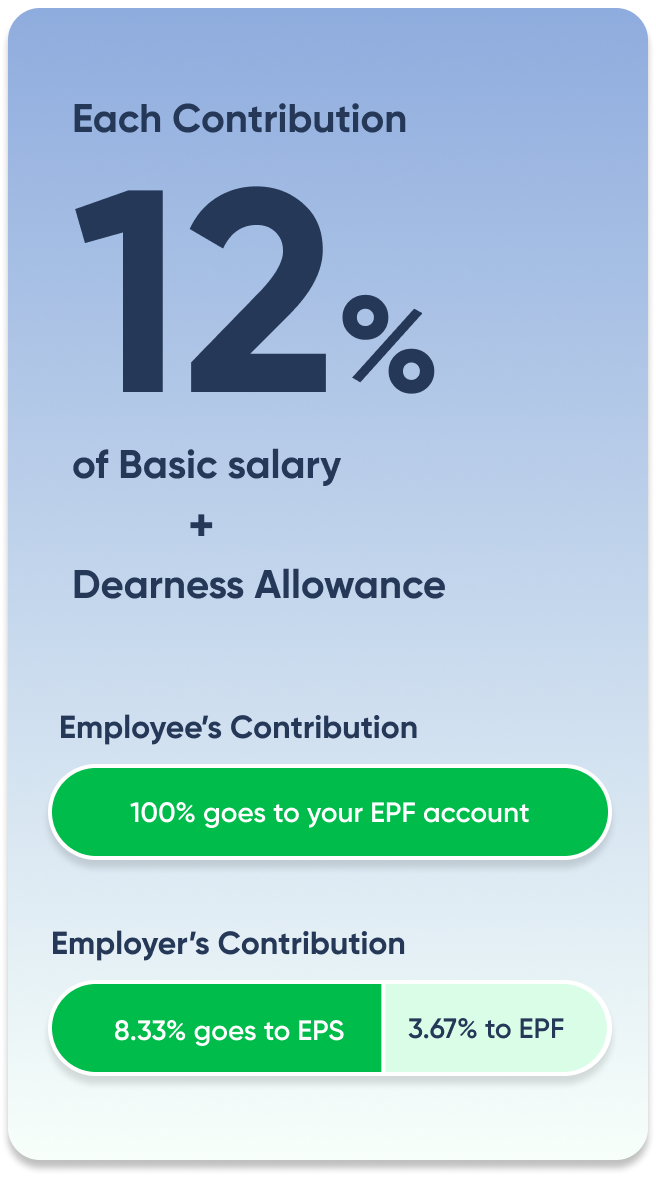

EPF thrives on a simple but powerful structure: shared responsibility and compounding growth.

Employee contribution: 12% of basic salary + DA, deducted each month

Employer contribution: Another 12%, split between EPF and EPS

Interest compounding: Annual compounding ensures you earn returns on both principal and

accumulated interest

The effect of compounding

is best appreciated over long durations. Over a 25-30-year career, even

modest contributions can snowball into a corpus that provides real financial independence in

retirement.

Accessing Your EPF: Withdrawals and Flexibility

EPF balances are primarily meant for retirement, but they can also serve as a financial cushion

during your working life. The EPFO allows both partial and full withdrawals depending on your

situation.

Partial withdrawals can be made online through the Member e-Sewa portal for needs such as housing,

children's education, marriage, or medical emergencies. You'll need your Aadhaar, PAN, and bank

details linked to your UAN. Once you submit a claim, funds are usually credited within 10 - 15 working

days. For those preferring the traditional route, Form 31 can still be submitted offline through the

employer.

Full withdrawal is permitted after retirement at age 58 or after two months of unemployment. If

you've left your job but haven't withdrawn, your EPF account continues to earn interest for up to

three years, preserving your savings.

Withdrawals and

Flexibility

EPF may have started as a retirement fund, but it's evolved into something more practical for

today's workforce. Over the years, rules have been relaxed to help members access their savings

during key life moments without derailing their long-term goals.

You can make partial withdrawals for buying or building a home, children's education, marriage,

or medical emergencies. Full withdrawal is now allowed after 12 months of unemployment, and

pension withdrawals can be made after 36 months of leaving service. Even if your account becomes

inactive, it continues to earn interest.

The latest 2025 updates have made the process simpler and more flexible

The old 13 withdrawal clauses

are now grouped into three broad categories:

Essential needs

Housing

Special situations like job loss

You can now withdraw from both employee and employer contributions, not just your share.

For housing, up to 90% of the EPF balance can be used after just 3 years

of membership

(earlier it

was 5).

A minimum 25% balance must stay invested to protect your retirement

savings. Partial

withdrawals can be made after just 1 year of service in many cases.

These changes recognise that financial needs don't always wait until retirement; they make EPF more

responsive to real life while still keeping its core purpose intact: long-term financial security.

Why EPF still matters

EPF may not be the most glamorous investment, but it remains unmatched in stability, predictability, and

long-term reward for disciplined saving. In an era of volatile markets, it continues to serve as the

bedrock of retirement planning for millions

FeatureWhy It Matters

Compulsory contributionsEnsures regular saving, even if you're not naturally disciplined

Employer contributionDoubles your savings pace without extra effort

Government - backedVirtually no default risk

Tax benefits under 80CReduces taxable income while building wealth. EEE category

Partial withdrawalsOffers flexibility for key life milestones

In essence, EPF acts as the “non-negotiable” foundation of any salaried professional's financial plan,

something you can rely on even if other investments fluctuate.

EPF vs Other Retirement Instruments

To understand EPF's relevance, it helps to compare it with other retirement options in terms of return

stability, liquidity, and tax treatment.

NPS9-12%Triple Tax benefitLocked till age 60 or 15 years tenure0.01-0.30%

Mutual Funds (ELSS)10-15%80C (upto 1.5 lakhs)

on investment in ELSS onlyAnytime1-2%

Fixed Deposits6-7%80C upto 1.5 lakhsLimitedNil

While EPF's returns may appear modest compared to market-linked instruments, its predictability and

safety make it a cornerstone of a balanced retirement portfolio.

How to Maximize EPF Benefits

To make EPF work harder for you, consistency and strategy matter more than timing or tinkering.

Maximize your contributions - Stick to the full 12%

contribution; avoid

voluntary

reductions

Encourage employer compliance - Ensure your employer

contributes regularly and

correctly

Monitor your account - Use the EPFO portal to check

balances, interest credits, and

withdrawals

Plan partial withdrawals carefully - Use only for

key life

events, not for short-term

liquidity

Combine with NPS or PPF - Diversify your retirement

plan for better

inflation-adjusted returns

Preserve continuity - When changing jobs, always

transfer your EPF to avoid

breaking

the compounding cycle

EPF isn't just a savings product; it's a social safety net built into India's salaried economy.

It

supports over 6 crore members, collectively holding more than ₹18 lakh crore in assets making it one of the largest

retirement

systems in the world. For most employees, it represents the one

financial habit that never falters, even when life gets busy.

Average annual returns have consistently hovered between 8-8.5%,

comfortably beating inflation for

most of the past decade. More importantly, employer contributions can add 20-30% extra to your

corpus over your working life, a quiet but powerful accelerator of retirement wealth.

Key Takeaway

EPF continues to be one of India's most effective and time-tested retirement

instruments.

It rewards consistency, builds discipline, and offers the peace of mind that comes with

government-backed safety. In a financial landscape full of noise and volatility, it remains

refreshingly

simple to save regularly, stay invested, and let time and compounding do the rest.

Retirement is not the end of earning

- it's the beginning of living on your own terms

India is at a turning point. A growing middle class, longer lifespans, and rising aspirations mean

that how we plan for our later years has never mattered more. Yet most of us are underprepared.

PensionBazaar exists to close that gap - with clarity, simplicity, and the right plan for every

stage of life. Your future self deserves nothing less.

.png)

.png)

Applicable to employees aged 18 to 58 years

Applicable to employees aged 18 to 58 years