The National Pension System (NPS) is a low-cost, tax-efficient way to build your

retirement corpus. With professional fund management and flexible options, it helps you grow

your

savings steadily and secure your financial future with ease.

Start Planning Now

Everything You Need To Know About The National Pension System

Retirement planning is easier when you start early. NPS or the National Pension System is the government's

longest-running effort to build a habit of long-term savings across the country. It is a market-linked

retirement plan where contributions are invested in a mix of equity, corporate bonds, and government

securities managed by professional Pension Fund Managers to grow your savings steadily over time.

Regulated by the Pension Fund Regulatory and Development Authority (PFRDA), NPS is low-cost, tax-efficient,

and now more flexible than ever, helping individuals - whether salaried, self-employed, or freelancers -

9systematically accumulate a retirement corpus while balancing growth and risk.

This instrument enforces the discipline needed for compounding to work its magic. It comes at the lowest

possible charges, or what one might call an expense ratio. It falls under the EEE (Exempt-Exempt-Exempt)

category - giving you a rare edge by keeping your returns completely free of capital gains tax.

Let's take a look at its key features:

Power of Compounding

Even small, regular contributions grow exponentially over time

because

your returns start earning returns, turning modest savings into a substantial retirement

corpus

over decades

Lowest Costs

Fund management fees just 0.01 - 0.09% vs 1 - 2% for mutual funds

Tax-free at all stages (EEE)

Contributions, growth, and partial withdrawals are tax-efficient

Greater Flexibility(2025 reforms)

Option for exit after 15 year tenure, 100% equity under MSF,

multiple

PRANs under one PAN and the option to withdraw 80% lumpsum

Equity + Debt Mix

Balanced growth and safety over time

NPS 2.0: More Flexible, More Personalized

The National Pension System has undergone significant updates in 2025 to provide more

flexibility

and personalization options for subscribers. These changes make NPS more accessible and tailored to

individual

needs.

Subscribers can now enjoy greater flexibility in investment choices, with expanded options

for

asset allocation and more personalized portfolio management. The system now offers enhanced features for

tracking and managing your retirement savings.

The new updates also simplify the account opening process and provide better support for

subscribers throughout their NPS journey. With these improvements, NPS continues to be one of the most

comprehensive retirement planning solutions available.

Whether you're just starting your career or planning for retirement, the updated NPS 2025

offers

features that can help you build a secure financial future.

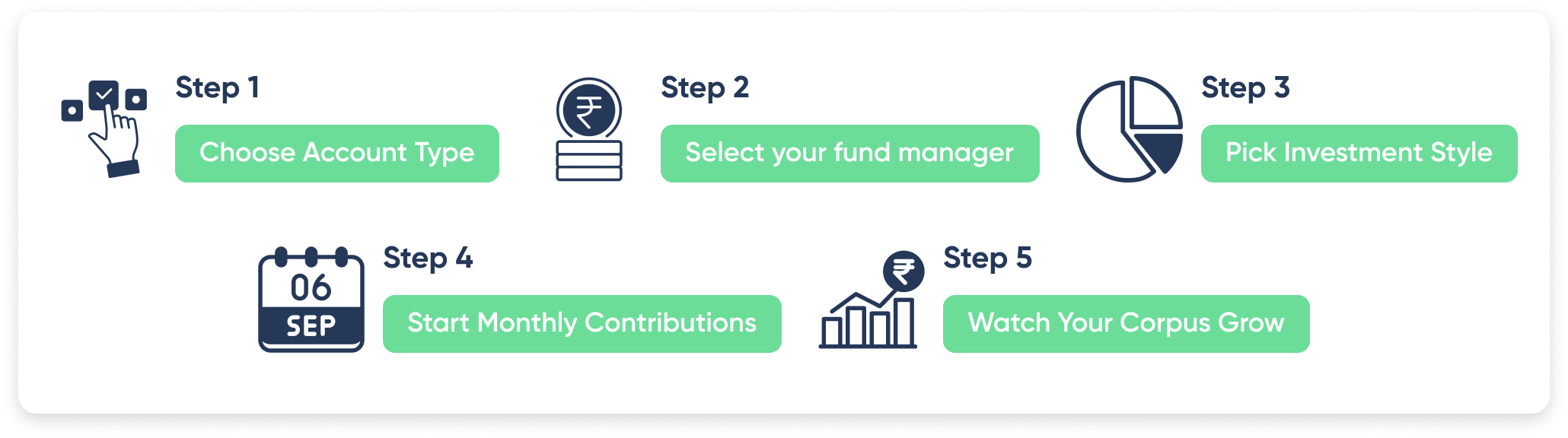

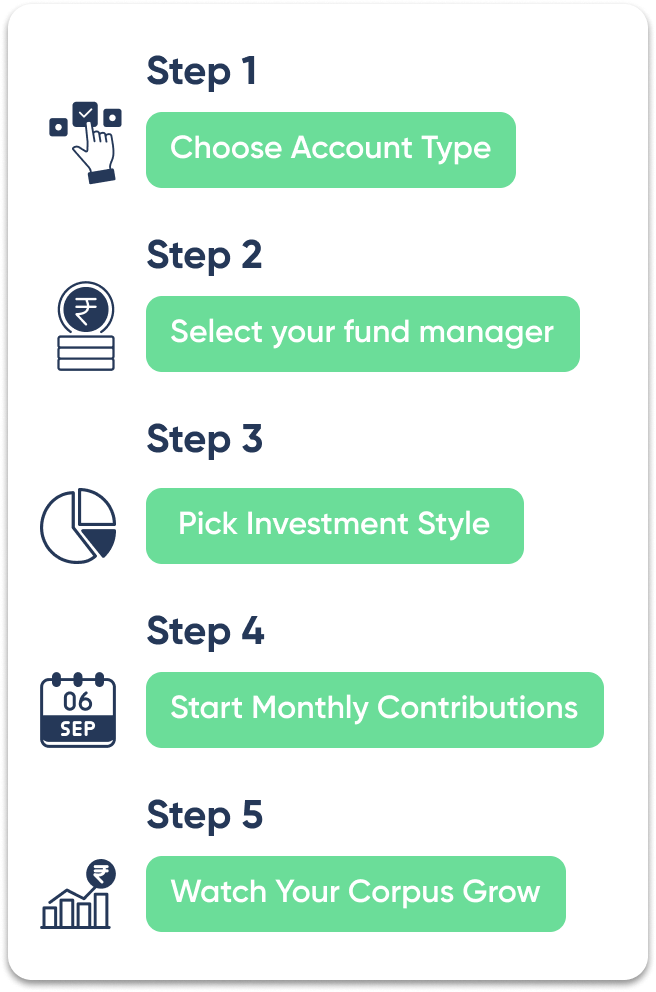

How to Open an NPS Account and Select the Right Options

You can start your NPS journey on nps.pensionbazaar.com in less than a minute, with a fully

digital and hassle-free account opening process. Opening an NPS account is simple and open to anyone

between 18 and 85 years, including salaried employees, self-employed professionals, freelancers, and

NRIs. All that's required is basic KYC documentation, such as a government-issued ID and address proof.

Your Permanent Retirement Account Number (PRAN) stays with you for life, allowing you to continue

contributing seamlessly even if you change jobs, move cities, or relocate abroad.

Step 1: Choose Your Account Type

Tier I - Retirement-focused (Mandatory): Offers tax

benefits

and enforces

long-term discipline. Partial withdrawals are allowed for specific life events such as

education,

marriage, illness, or buying/construction of a home.

Tier II - Flexible savings (Optional): Offers full

liquidity

with no tax

benefits; ideal for short- or medium-term savings.

Step 2: Choose Your Pension Fund Manager (PFM)

Pick from 10 trusted Pension Fund Managers such as HDFC Pension Fund,

ICICI

Prudential Pension Fund, SBI Pension Fund, Aditya Birla Sun Life Pension Fund, Kotak

Mahindra

Pension Fund, Axis Pension Fund, LIC Pension Fund, DSP Pension Fund, Tata Pension Fund,

or UTI

Pension Fund. With the new Multiple Scheme option, you can invest across several fund

managers

while

still tracking all your savings under a single Permanent Retirement Account Number

(PRAN).

Step 3: Choose Your Investment Style

Auto Choice (Lifecycle Fund): A hands-free, age-based

allocation that automatically adjusts your money mix between equity and debt as you grow

older -

taking higher risk when you're young and becoming safer as you near retirement. Types of

Auto

Choice

Funds

Life Cycle 25(Low) - Equity exposure starts at 25% and tapers to

around 5%

by age 55

Life Cycle 50(Moderate) -Equity exposure begins at 50% and reduces

to 10%

by 55

Life Cycle 75(High) -Equity starts at 75% and gradually drops to

15% by 55

Life Cycle Aggressive (formerly Balanced Life cycle Fund) - Equity

starts

at 50% and gradually

drops to 35% by 55

Active Choice: Gives full control over your equity,

corporate

bonds, government securities, and alternative asset allocation. Under 2025 reforms, you

can now

go

up to 100% equity under MSF, giving experienced investors higher growth potential if

they can

tolerate short-term volatility. Annual rebalancing is still available, and now you can

rebalance

across schemes under the same PRAN

Multiple Scheme Framework(New) : MSF lets you

invest in

multiple pension

schemes under a single PRAN, enabling better diversification across fund managers and

strategies.

With the 2025 reforms, MSF also allows up to 100% equity allocation under eligible

schemes,

maximising long-term growth potential for investors who can handle market volatility.

You can

seamlessly rebalance across schemes, whether you follow Auto or Active Choice, without

opening a

new

account.

How Does NPS Work?

The National Pension System (NPS) is a government-regulated, long-term retirement framework

designed to help you build a pension corpus in a systematic way. When you open an NPS account, you are

assigned

a Permanent Retirement Account Number (PRAN), which

remains with you for life, even if you change jobs or

locations.

You make regular contributions to your NPS account during your working years. These

contributions

are invested across equity, corporate debt, and government securities based on the investment choice you

select,

and are professionally managed by Pension Fund Managers (PFMs) appointed by the NPS regulator.

NPS follows a defined retirement structure. On retirement, a portion of the accumulated

corpus

can be withdrawn as a lump sum (up to 80%, with 60% being tax-free), while the remaining amount is

mandatorily

used to purchase an annuity. This annuity provides a steady monthly pension, ensuring a regular income after

retirement.

By combining regulated fund management, flexible investment choices, and a structured payout

at

retirement, NPS offers a transparent and disciplined approach to building long-term retirement income.

Example :

Contributing ₹5,000/month from age 30 can grow to ₹1.5 crore by

age 60, thanks to your contributions and the returns they earn over 30

years.

Doubling the contribution to ₹10,000/month but starting at age 40

results in a lower corpus of ₹92 lakh by age 60.

This demonstrates that starting early and investing consistently allows even

small amounts to grow exponentially, as the returns themselves generate additional returns—a

true snowball effect for your retirement wealth.

*Assuming 12% annualized returns. Figures are for illustration

only;

actual results may differ.

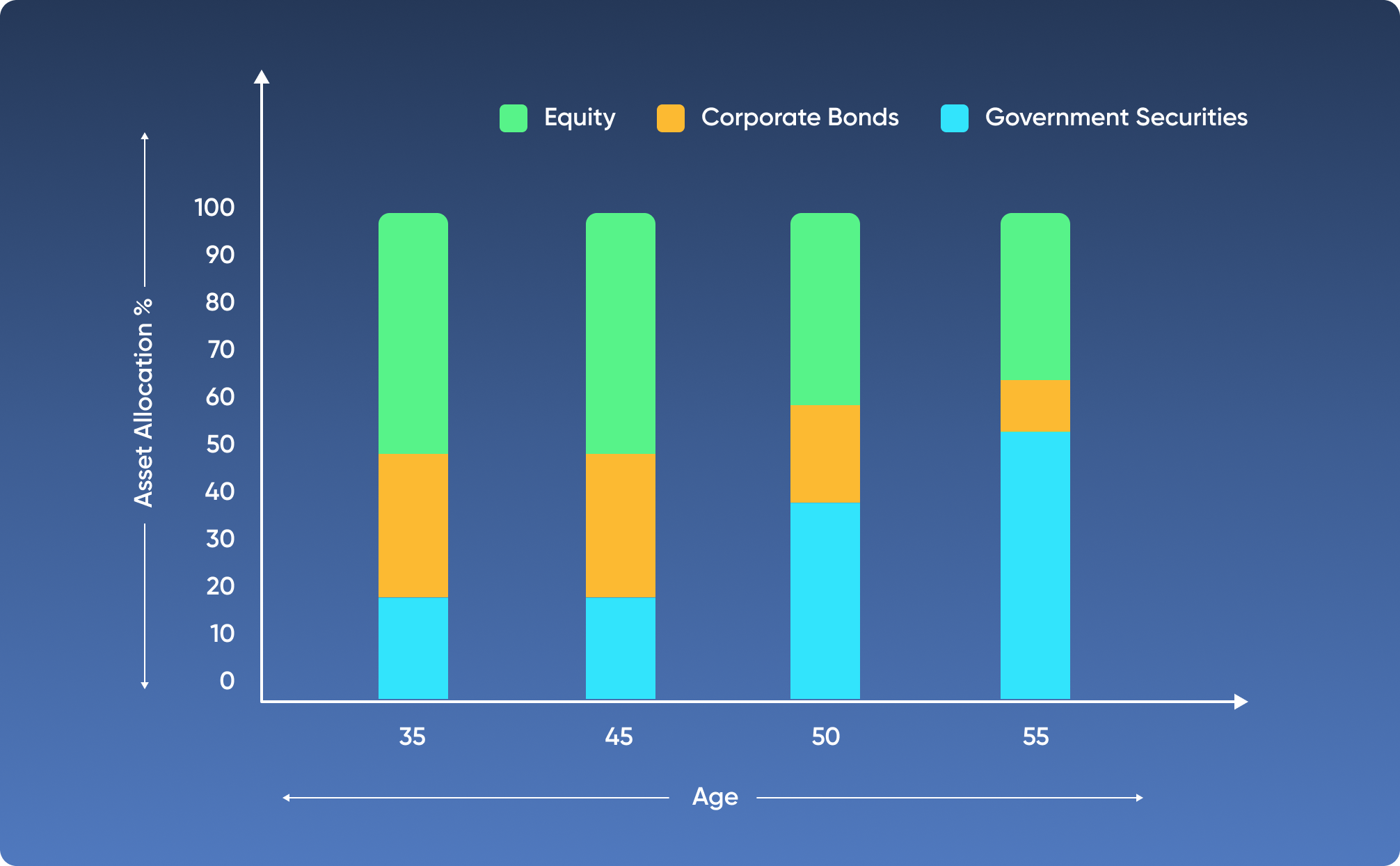

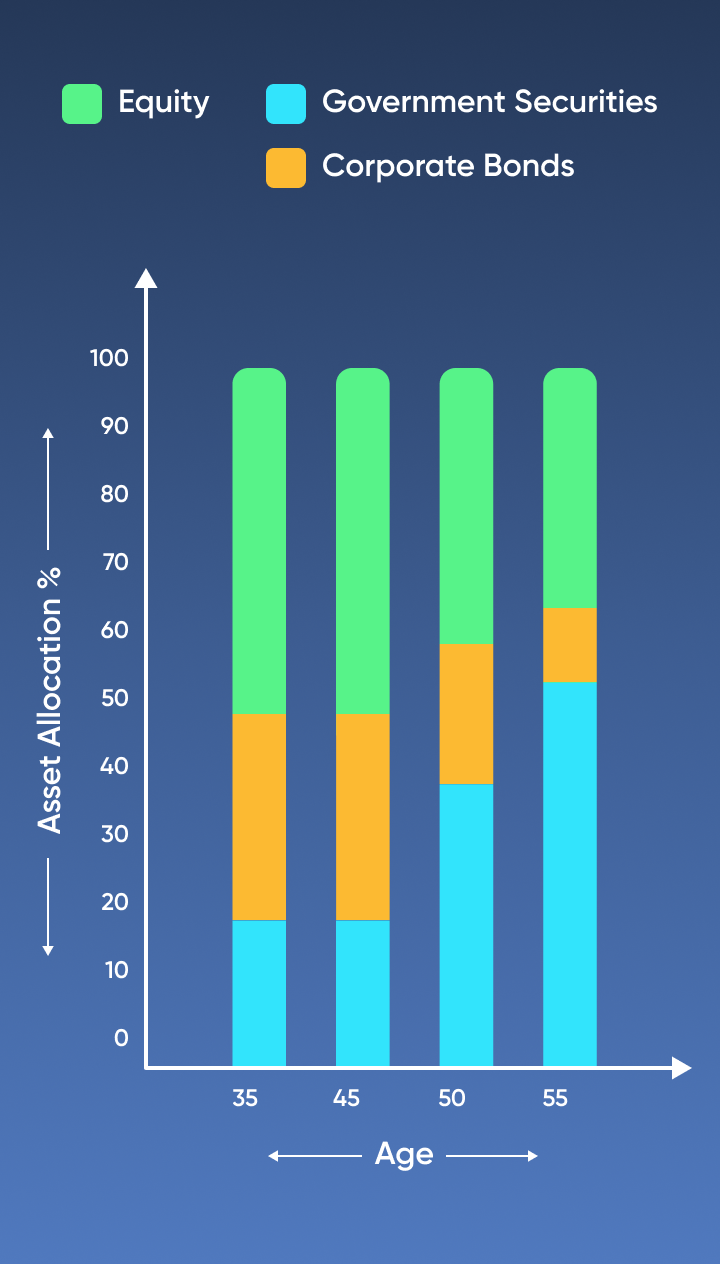

Asset Allocation Evolution

NPS offers two distinct ways to manage your investments -Auto Choice and Active Choice,

giving

you the freedom to decide how involved you want to be in managing your portfolio.

Auto Choice - Lifecycle Fund:

Auto Choice adjusts your portfolio automatically as you age, shifting from equity-heavy

growth in

your 30s to safer bonds and government securities by retirement, balancing growth with risk. There are four

types of Lifecycle Funds based on your risk appetite like LC75 (High), LC50 (Moderate), LC25 (Conservative)

&

Balanced Life Cycle Fund.

For example, in the Balanced Lifecycle Fund (LC100), the allocation evolves with age -

starting

with 50% in equity, which gradually reduces to 35% by age 55, ensuring a smooth transition from growth to

stability.

Active Choice - Manual Allocation:

Active Choice lets you control your allocations manually, maintaining higher equity or

adjusting bonds as you see fit. This approach is ideal for those who want flexibility and can handle

market

swings. Under the 2025 reforms, your investment options gain more flexibility and growth potential, with

Auto/Active Choice now compatible with multiple fund managers and Active Choice allowing up to 100%

equity

where suitable.

Auto/Active Choice now works with MSF, allowing diversified allocation across multiple PFMs

Active Choice can now leverage 100% equity for higher long-term growth, where suitable

Returns, Costs, and Tax Benefits

Returns (5-Year Annualised):

NPS is designed to deliver steady, market-linked growth over time. Equity-focused schemes

have

historically generated around. 14-16% per year, offering higher growth potential over the long term.

Corporate

bond schemes provide 6-7% annualised returns, balancing risk with moderate income, while government

securities

yield 5-6%, prioritising capital protection and stability. These returns reflect past performance and are

linked

to the performance of the underlying assets, highlighting the advantage of a diversified, professionally

managed

portfolio.

*Source NPS Trust. Returns as on 29th Oct'25.

Tax Benefits:

NPS remains one of the few retirement instruments offering triple tax benefits (EEE -

Exempt-Exempt-Exempt), meaning your contributions, the growth of your investments, and a portion of your

withdrawals are tax-efficient.

Contribution Type

Old Regime Deduction

New Regime Deduction

Personal Contribution

Up to ₹1.5 lakh under Section 80C

Not applicable

Additional NPS Contribution

₹50,000 under Section 80CCD(1B) (over 80C)

Not applicable

Employer Contribution (Corporate NPS)

Upto 10%(private)/14%(govt) of salary under Section 80CCD(2)

Up to 14% of salary (Basic + DA) under Section 80CCD(2) (This is the only NPS

benefit

under new regime)

Withdrawals & Retirement Options

NPS offers a structured yet flexible approach to accessing your retirement savings, balancing

long-term security with immediate financial needs. At retirement , you can now withdraw upto 80% of your

corpus of which 60% is tax-free, while the remaining portion is used to purchase an annuity. Even before

retirement, you can access a portion of your funds for important life events, with partial withdrawals of up

to 25% now proposed to increase upto 4 times, offering greater flexibility without compromising long-term

growth. Here are the key takeaways:

80% lumpsum withdrawls of which 60% of corpus can be withdrawn tax-free

Only 20% must be used to buy an annuity

Up to 25% of contributions can be withdrawn before retirement for specific needs - now proposed to

increase upto 4 permitted withdrawals

Comparing NPS with other retirement and investment options helps you make an informed

decision about

your

retirement planning

strategy.

Product

Return

Tax Benefit on Investment

Tax benefit on Maturity

Liquidity

Costs

NPS (Post-Reforms)

Upto 16%

Exempt (u/s 80 C, 80 CCD(1B), 80 CCD(2)

Partially taxable

Lock-in till age60 or 15 years (MSF)

0.01-0.30%

EPF

8.25%

Exempt (up to 1.5 L u/s 80C)

Tax-free

On job change/retirement

Nil

PPF

7.1%

Exempt (up to 1.5 L u/s 80C)

Tax-free

15-year lock-in

Nil

Mutual Funds

10-12%

Taxable (Select MFs exempt)

Taxable

Anytime

1-2%

FDs

6-7%

Taxable

Taxable

Limited

Nil

Is NPS Right for You?

If you value discipline, diversification, and compounding, NPS offers one of

the

most cost-effective retirement solutions in India - now upgraded with flexibility, MSF, and

higher growth potential through the 2025 reforms.

NPS has evolved from a rigid pension plan to a modern, modular,

investor-friendly

retirement solution. Start small, stay consistent, and let compounding and smart asset

allocation secure your financial independence.

NPS Variants

NPS VatsalyaA government-backed option designed for senior citizens or risk-averse investors. It focuses

on

lower-risk investments while still offering steady, market-linked growth over time

Atal Pension

Yojana (APY):Specifically for workers in the unorganised sector, APY guarantees a fixed monthly pension at

retirement. The government may co-contribute for eligible participants, making it an accessible

retirement option for lower-income individuals

Corporate NPS:Offered through employers, this variant allows contributions from both the employee and the

employer. Employee contributions are eligible under Section 80CCD(1B), while employer

contributions

get tax benefits under Section 80CCD(2), making it a structured and tax-efficient way for

salaried

professionals to build retirement savings

FAQs About Nation Pension System

Q. Can NRIs invest in NPS?

Yes, non-resident Indians can open an NPS account by completing basic KYC and

providing a PAN. The account remains portable even if you move across countries.

Q. Can I switch Pension Fund Managers (PFMs)?

Yes, you can change your PFM once a year to align with your risk appetite,

investment style, or fund performance.

Q. Can I have multiple NPS accounts?

Under the new Multiple Scheme Framework (MSF), you can hold multiple schemes

under the same Permanent Retirement Account Number (PRAN), enabling diversification across

different fund managers and asset allocations.

Q. What happens if I change jobs or cities?

Your NPS account is fully portable, so contributions continue seamlessly

regardless of job changes, relocations, or even moving abroad.

Q. Are there limits on contributions?

Tier I has minimum contributions to remain active, while Tier II is fully

flexible. The reforms do not change contribution limits but enhance flexibility in

withdrawals

and investment options.